Korea VAT and Tax for Foreign Shippers: A 2026 Guide

When you ship goods into South Korea as a foreign company, you owe 10% VAT at the border and an average 8% customs duty on shipments above USD 150. The tax obligation itself is simple — but who files it (your overseas entity, a Korean IoR partner, or a Korean subsidiary) is the structural decision that drives everything downstream, from Coupang seller onboarding to KC certification to whether you can list at all.

That is the question most "Korea VAT" articles never get to. They stop at the rate.

The short answer on Korea VAT and customs

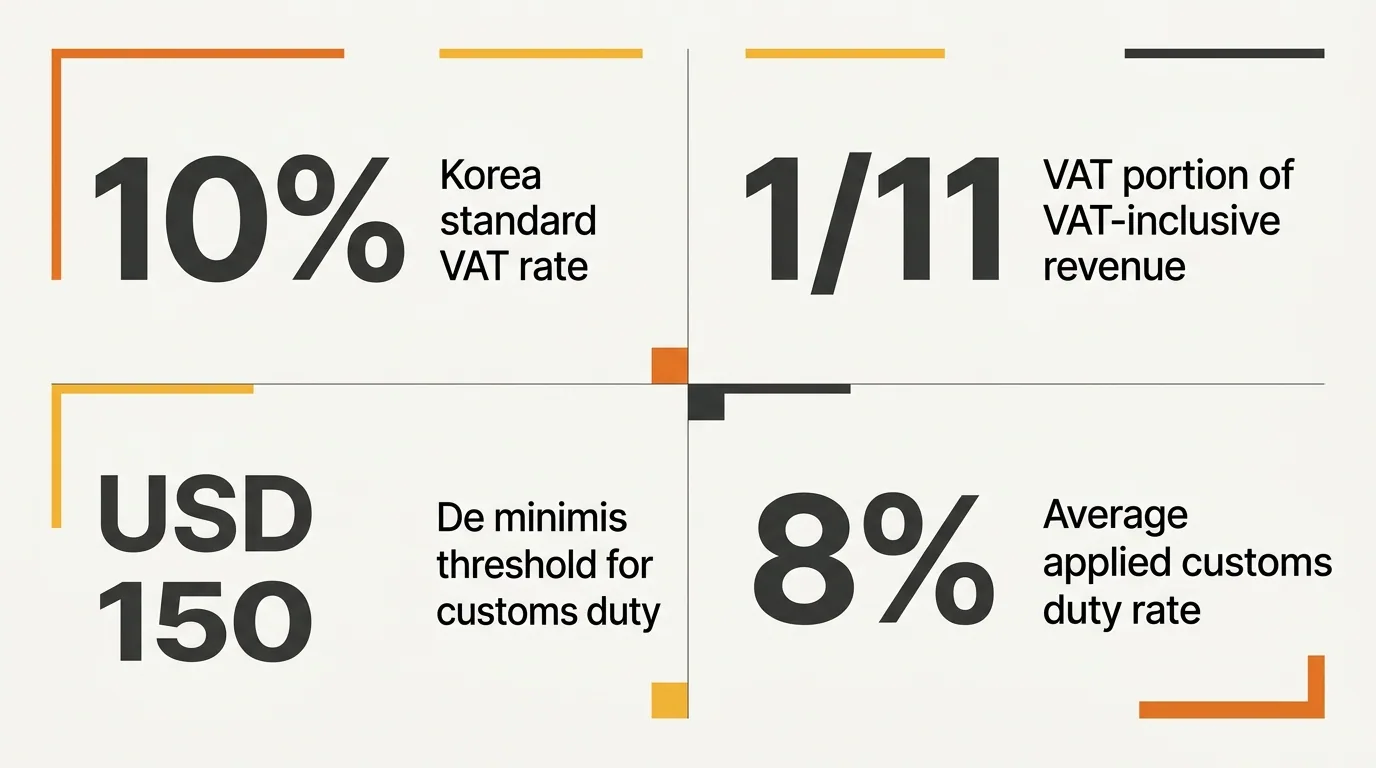

The short answer is this. Korea applies a single standard VAT rate of 10% on the supply of goods and services, including imports. For VAT-inclusive revenue, the VAT portion equals 1/11 of the gross figure — about 9.09%. Shipments valued at or above USD 150 cross the de minimis threshold and are subject to customs duty as well, with the average applied rate landing around 8% but ranging widely by HS code.

VAT is collected at the border by Korea Customs Service (관세청) when goods clear customs, and again on the downstream sale. The party listed as the Importer of Record on the customs declaration is the party that pays the import VAT and customs duty up front. That party also receives the import VAT credit when it later files its VAT return with the National Tax Service (국세청). If you are shipping from abroad with no Korean entity and no IoR partner, you cannot reclaim that import VAT — it becomes a cost.

This is the part the tax-summary pages tend to gloss over. The rate is simple. The cash-flow and credit logic depends entirely on entity structure.

Three ways foreign brands actually pay Korea VAT

In practice, there are three structural answers to "who pays VAT when my goods enter Korea."

Path 1: Cross-border, buyer-paid duty and VAT. The Korean consumer is the importer. They pay duty and VAT at the point of delivery via the courier. You, the foreign seller, never appear on a Korean tax return. This works for low-volume direct-to-consumer sales but breaks the moment you want to list on Coupang Rocket delivery or hold inventory in Korea.

Path 2: Importer of Record partner. A Korean entity — either a specialist Importer of Record provider or a managed operator like Kontactic — acts as IoR. That entity pays import VAT and duty, takes the input credit, and sells onward as the Seller of Record. The foreign brand never registers in Korea but still gets local inventory, Rocket delivery, and KRW pricing.

Path 3: Your own Korean limited company (유한회사). You establish a Korean entity, register it with the National Tax Service, and that entity is both IoR and SoR. You pay VAT, you reclaim VAT, you file quarterly. Maximum control, maximum administrative load.

Each of these has very different implications for Coupang access, marketing budget control, and how easily a tax officer can come back to you with questions. We unpack them at length in our Spark vs. Flame vs. Blaze comparison.

The numbers you actually need at the border

Before we get into Coupang and PDPs, fix four numbers in your head. These are the figures we quote when scoping projects with foreign brands.

- 10% — the standard VAT rate on imports and most domestic supplies.

- 1/11 — the VAT portion of any VAT-inclusive revenue figure (so KRW 11,000 gross = KRW 1,000 VAT).

- USD 150 — the de minimis threshold above which customs duty starts to apply on most goods.

- 8% — the average applied customs duty rate across Korean imports, though your specific HS code can land much higher or lower.

These four numbers come up in every Korea landed-cost conversation. They are also the ones that travel cleanly between PwC's tax summary, Korea Customs Service, and what we see in actual import filings.

In our experience, the trap isn't the rates themselves — it's the second-order costs that hang off the IoR decision. Customs broker fees, KC certification, Coupang platform fees, and Rocket Growth (로켓그로스) storage and returns handling are where the real margin compression happens. We break those down further in our DDP landed-cost guide and in the breakdown of who pays what in Korea.

Where the tax question collides with Coupang

This is the angle the PwC and FedEx-style pages skip. Coupang doesn't care about your tax theory — it cares about whether the entity onboarding to the Main Seller Account can be invoiced for VAT-inclusive platform fees and can issue VAT-compliant tax invoices (세금계산서) to consumers when required.

Practically, that means:

- A pure cross-border seller cannot run Coupang Rocket delivery. Rocket requires inventory inside Korea, which requires a Korean IoR.

- An IoR partner sells under their own Main Seller Account. You don't appear on the listing as the seller of record. For most brands this is fine; for some — particularly fashion or premium beauty — it is not. We've written separately about the trade-off between IoR-only and a local entity for skincare brands.

- A Korean entity of your own can register its own Coupang account, but the entity setup itself has gotten meaningfully harder in 2026. Tax-office pushback and bank account refusals now stretch what used to be a 4–6 week process. We covered that in detail in the May 2026 tax-office crackdown post.

VAT compliance, in other words, is not separable from the seller account. The same entity that files your VAT return is the entity Coupang invoices, the entity the customer sees on the receipt, and the entity that holds the settlement funds. Picking your tax structure is picking your commerce structure.

The PDP is part of your tax-paid margin math

A foreign brand that pays 10% VAT, an 8% average duty, Coupang's selling commission, and Rocket Growth handling fees has roughly 25–35% of gross stripped out before margin starts. The only operational lever left is conversion rate. In Korea, that lever is the Product Detail Page.

A Korean PDP is a long-scroll, image-heavy mobile experience — typically 20,000 pixels of vertical canvas. It combines localized claim framing, hero comparison shots, and trust signals (KC mark, MFDS approval, country-of-origin badges) as embedded graphics, not text. The text-only listing that ships with most import-agent packages converts at a fraction of the rate.

This matters for tax-paid economics because the only way to absorb the VAT and duty stack and still grow is to convert better than the cross-border baseline. Brands that ship inventory locally but treat the PDP as an afterthought usually underperform their old cross-border numbers for the first two quarters. We've watched it happen often enough that it shapes how we sequence launches — see our note on operational readiness before ad spend.

“VAT is the easy part. The hard part is making sure the entity that pays it can also list, ship, and convert in Korea — those three are one decision, not three.”

Kontactic team — Operations note

KC certification: the compliance layer most VAT articles skip

Customs will sometimes clear a shipment without confirming category-specific certifications, and brands take that as a green light. It isn't. The Korea Customs Service can release goods that the Ministry of Trade, Industry and Energy or the Ministry of Food and Drug Safety later flag as non-compliant. The economic owner of those goods — usually you — bears the cost of recall or destruction.

Categories that almost always require pre-import certification:

- Electrical and electronic products → KC certification (KC 인증), often a mix of electrical safety, EMC, and radio. See our note on when a foreign EMC report can support a Korean Declaration of Conformity.

- Food and food-contact items → MFDS import declaration, sometimes pre-registration. See importing food and hygiene products into Korea.

- Pet food → APQA feed registration. See the Korea pet food entry guide.

- Cosmetics → MFDS Functional review where applicable, plus a registered Responsible Person.

A VAT-paid shipment is not a compliant shipment. Customs clearance and product-category certification are separate gates. Both must be cleared before you list on Coupang.

KC and MFDS costs sit on top of the 10% VAT and the customs duty. They don't appear on the tax summary pages because they are technically not taxes — but operationally they are part of the same landed-cost decision. The Korea entry budget guide lays out where they typically land.

Entity setup and how to think about the next step

For brands that want to own the customer relationship, the seller account, and the bank account, a Korean limited company (유한회사) is the right answer. It is also the slowest and most administratively expensive answer, and it has gotten harder for non-resident foreigners in the last 18 months — tax offices now scrutinize virtual offices, minimal capital, and absent CEOs. We walked through the current path in our note on setting up a Korean entity as a non-resident and in the corporate bank account piece.

For brands that want speed to first sale and are willing to operate under a partner's IoR and SoR, the cleaner answer is a managed IoR arrangement. VAT, customs, and Coupang sit with the partner. You ship DDP, fund inventory and ads, and own the brand.

The honest framing — and the one we use internally — is that the right structure depends on where you are in the demand curve. If you have Korean cross-border buyers already and you want to capture that demand fast, IoR is usually correct. If you are building a long-term Korean P&L and want full control, the entity path is correct. Both are legitimate. Each has trade-offs you need to weigh carefully.

If you take one thing from this article, take this: the 10% VAT number is not the decision. The decision is which entity sits on the customs declaration, the Coupang account, and the tax invoice. That entity choice locks in your speed to launch, your margin profile, your KC scoping, and how much of the PDP work you keep in-house.

If you want to validate Korean demand before committing to an entity, run cross-border first and look at the engagement signal — we wrote about that in why cross-border orders understate your Korea opportunity. If you already have that signal, the question becomes operator selection.

Scope your Korea VAT and entry structure with Kontactic

We help foreign brands choose between IoR-only, full Korean entity, and managed-entity setups — and handle VAT, customs, Coupang onboarding, KC scoping, and the localized PDP under one operator.

About the author

Korean and global e-commerce operators with 15+ years of cross-border experience, led by CEO Isaac Lee — KOTRA-certified consultant and official lecturer for Seoul City and the Korea Customs Service. We run Korea market entry for Western brands every day; this blog documents what we learn in the field.

More about Kontactic →Related Articles

Who Is the Importer of Record When You Sell on Coupang?

When you sell locally on Coupang, the Importer of Record must be a Korea-resident party accountable to the Korea Customs Service — not Coupang, and not your freight forwarder. Here is why.

Is Your Air Freshener a "Biocidal Product" in Korea?

In Korea, whether your air freshener, cleaner, or repellent is a regulated biocidal product depends on its active substance and function — not its shelf category. Here is how to sort which bucket yours falls into.

Is Your Product a "Children's Product" Under Korean Law?

If a product is intended for use by children roughly age 13 and under, Korean law classifies it as a children's product (어린이제품) and pushes it onto a stricter, separate KC certification regime under KATS.