Q1 2026 Coupang–Naver Shift: Your Channel Strategy

The Q1 2026 numbers from Korea's two largest ecommerce platforms reset the channel-mix conversation. Coupang took a customer-trust hit in December 2025, growth slowed sharply, and Naver SmartStore (스마트스토어) absorbed real volume during the same window. For brands planning a 2026 entry, the practical takeaway is this: Coupang remains the right primary channel for most Western brands, but a parallel SmartStore presence is no longer optional — it is the hedge against single-platform trust risk.

This is a channel-mix decision, not a platform switch.

What the Q1 2026 numbers actually say

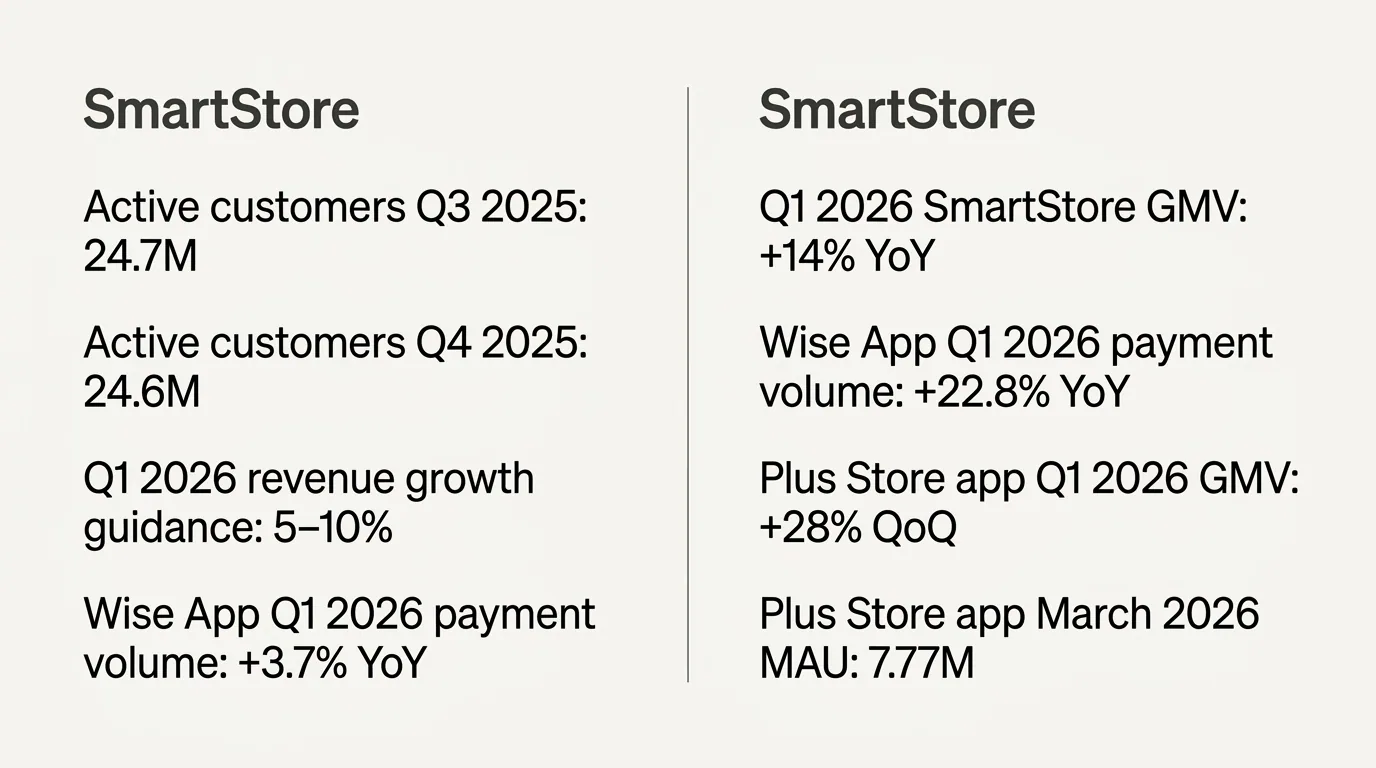

Coupang disclosed a major customer data incident in December 2025. The aftermath shows up cleanly in the data. Active customers slipped from 24.7M in Q3 2025 to 24.6M in Q4 2025 — the first sequential decline since 2023. Product commerce constant-currency revenue growth, which had been running near 18% in Q3 2025, decelerated to roughly 12% in Q4 2025 and then to about 4% in January 2026 before recovering through February and March. Q1 2026 revenue growth guidance came in at 5–10%, well below the prior trajectory.

Profit metrics moved with it. Q4 2025 adjusted EBITDA was $267M, down roughly 37% year-over-year, and operating profit was $8M, down about 97% year-over-year. The deceleration was real, but it was a customer-trust shock concentrated in a defined window — not evidence that the underlying logistics moat had cracked.

By March 2026, the recovery was visible. Coupang's monthly estimated payment volume reached KRW 5.71T (+12% month-over-month), and MAU was 33.45M (+1% MoM) — the first rebound, with both numbers approaching pre-incident levels.

Where the volume went

Naver did not just sit there. SmartStore Q1 2026 GMV grew +14% year-over-year. Independent panel data tells a sharper version of the same story: Wise App's Q1 2026 estimated payment volumes show Coupang at +3.7% YoY versus Naver at +22.8% YoY. The gap in growth rates during the quarter is the headline number to internalize.

Naver also reorganized how it reports the business. From Q1 2026 onward, commerce is no longer broken out as a separate segment — it is folded into a combined "Platform" segment alongside search and display advertising. That makes year-over-year comparisons harder by design. But the operational signals are clear enough.

The Naver Plus Store app (네플스 앱), which is the consumer-facing layer Naver has been pushing as its dedicated shopping destination, posted Q1 2026 GMV +28% quarter-over-quarter, with March 2026 MAU of 7.77M. The investment direction — a dedicated app, an AI shopping agent, and a fulfillment program in N-delivery (N배송) — is structural, not a one-quarter promotion.

Read it as a trust shock, not a structural shift

The temptation, looking at this data, is to overcorrect. We don't think that's the right read. Coupang's logistics infrastructure, Rocket delivery network, and Rocket Growth (로켓그로스) fulfillment program are still the most efficient way for a foreign brand to scale unit volume in Korea. The customer base recovered most of the way back within a quarter. None of the platform-level economics that make Coupang the default entry channel — high MAU, dense fulfillment, conversion-grade ad inventory — got worse.

What did change is concentration risk. A foreign brand running Korea on a single Coupang storefront a year ago carried operational risk (account suspension, listing merges, item matching disputes). Today, that same brand also carries platform-level trust risk it can't control or hedge against from inside one channel. The way to address that is not to leave Coupang. It is to also be on Naver SmartStore, which is where a meaningful share of Korean shoppers spent the quarter while they reassessed.

The required framing here is the one we keep coming back to with brands evaluating Korea entry: Korean customers for these brands already exist. The question is which platforms they are sitting on now. Q1 2026 made the answer to that question more plural than it was in 2024.

Two-channel from day one. Plan SmartStore in parallel with Coupang, not after. The incremental setup cost during the initial Korean entity and listing build is far smaller than retrofitting a second channel a year later, when ops are already busy with Coupang growth.

What Coupang still does better

Be honest about the tradeoff before recommending the hedge.

Rocket Growth fulfillment is a single-tier 3PL relationship. Inventory goes from your forwarder into a Coupang-operated warehouse, and Coupang handles storage, last-mile, and returns under one roof. The ad mechanics on Coupang — sponsored search, conversion data feedback, automated bidding — are tightly coupled to that fulfillment layer. This coupling is why a well-run Rocket Growth listing converts at the rates it does. We've written about how this combination changes margin structure in how Coupang IoR and 3PL change your Korea margins.

For most Western brands with cross-border demand, that combination is still the fastest path from "we have Korean customers buying through us internationally" to "we have a real local Korean ecommerce business." The decision framework hasn't changed; we covered it in Rocket Growth vs cross-border selling in Korea and the underlying logic still holds.

Settlement is also more predictable on Coupang once you understand the cadence. The default is monthly, with weekly and fast-pay options at a discount; we walk through this in Coupang settlement timelines: monthly vs weekly vs fast.

Where SmartStore is messier

SmartStore's tradeoffs are not hidden. Worth naming them directly.

Ad mechanics. Naver's shopping ad ecosystem runs across search, Smart Channel, and the broader Naver content surface. Conversion attribution is harder to close cleanly than Coupang's in-platform sponsored search, and the ROAS curve for a foreign brand without Korean search authority takes longer to bend.

Operational burden. SmartStore is more self-service than Coupang. Listing creation, CS handling, returns, promotions — the seller's hands stay closer to the keyboard. For a brand running a thin local team, that's real ongoing labor.

N-delivery fulfillment is multi-tier. This is the one foreign brands underestimate most. N-delivery (N배송) is operated through Naver Fulfillment Alliance partners, who subcontract to downstream 3PLs. The structure: Naver sets the rules, an alliance partner is your contractual counterparty, and a third operator runs the warehouse and last-mile. Compared to Rocket Growth's single-tier Coupang-operated model, there are more handoffs, more potential SLA gaps, and more variability in returns processing. None of that is disqualifying. It does mean SmartStore fulfillment requires more active oversight than Rocket Growth.

What a two-channel launch actually looks like

For a foreign brand entering Korea in 2026 with validated cross-border demand, the practical sequence we'd recommend looks like this:

- Lead with Coupang for volume. Coupang remains the highest-conversion path to first KRW of local revenue, especially for categories where Rocket Growth fulfillment matters (small parcels, frequent reorder, repeat-purchase consumables).

- Stand up SmartStore in parallel during onboarding. While Coupang account creation, KC certification (KC 인증) where applicable, and Rocket Growth inbound are in progress, build the SmartStore storefront on the same Korean entity. Reuse Korean-localized product copy and assets. The marginal cost of a second listing is small; the marginal cost of building it 12 months later, with no ops bandwidth, is large.

- Decide on N-delivery deliberately. Don't default to N-delivery just because it exists. For early SmartStore volume, standard parcel shipping from your domestic 3PL is often fine. Move into N-delivery only when SmartStore order volume justifies the multi-tier overhead.

Throughout: treat the channels as one P&L — coordinate inventory pools, pricing decisions, and promotion calendars. Don't run two channel managers who don't talk to each other.

This is the same operational logic we apply when scoping any local Korean entity. The two-channel model fits cleanly into a Flame engagement (entity administration plus commerce operations on the client's own Korean entity) because both Coupang and SmartStore are managed under the same legal structure with the same Seller of Record.

For brands still earlier in the decision tree, the broader sequence is covered in how to sell on Coupang as a foreign brand. The framework hasn't changed; the channel mix downstream has.

Common questions

Should we pause Coupang plans because of the December 2025 incident? No. The active customer base, payment volume, and MAU all recovered substantially by March 2026. The platform economics for foreign brands have not changed.

Is SmartStore now bigger than Coupang for foreign brands? No. SmartStore grew faster in Q1 2026, but Coupang's absolute volume, fulfillment density, and conversion mechanics still make it the primary channel for most Western brands going local.

Do we need a Korean entity to sell on SmartStore? Yes, for the local SmartStore experience that Korean shoppers expect — the same logic that applies to Rocket Growth. Cross-border SmartStore exists but does not give you N-delivery or competitive shipping speeds. Most of why this matters is covered in why cross-border orders understate your Korea opportunity.

Can the same Korean entity hold both Coupang and SmartStore accounts? Yes. One Korean limited company (유한회사) is the Seller of Record on both platforms, files VAT under the same registration, and pools inventory across channels — assuming your 3PL setup supports it.

What if we're a smaller brand and can only run one channel well? Then run Coupang first, but build SmartStore foundations — domain, brand registration, basic storefront — during the initial entity buildout so the second channel is a launch decision later, not a setup project.

Ready to plan a two-channel Korea launch?

Talk to Kontactic about your 2026 Korea channel mix

If you have validated Korean cross-border demand and are deciding how to structure Coupang and SmartStore in parallel, we can walk through the entity, fulfillment, and operations sequence with your specific category in mind.

About the author

Korean and global e-commerce operators with 15+ years of cross-border experience, led by CEO Isaac Lee — KOTRA-certified consultant and official lecturer for Seoul City and the Korea Customs Service. We run Korea market entry for Western brands every day; this blog documents what we learn in the field.

More about Kontactic →Related Articles

Who Pays for What in Korea: Operating Costs Explained

Inventory, ads, platform fees, VAT — every Korea entry model puts these costs on the client. Here is exactly how funding flows under Spark, Flame, and Blaze.

Coupang Settlement Timelines: Monthly vs Weekly vs Fast

Coupang pays sellers on the 20th business day of the following month by default — close to 60 calendar days. Compare monthly, weekly, and fast settlement.

Selling Grills in Korea: Three Required Certifications

A cooking grill sold locally in Korea usually needs three separate certifications — electrical safety, EMC, and food-contact registration. Here is how each works.